by Russell Noga | Updated October 2, 2024

What Does Medicare Plan G Include?

Navigating the world of Medicare can be overwhelming, especially when it comes to understanding the various supplement plans available.

Navigating the world of Medicare can be overwhelming, especially when it comes to understanding the various supplement plans available.

Medicare Supplement Plan G is a comprehensive policy designed to fill most of the gaps in Original Medicare coverage, providing you peace of mind and financial stability.

In this article, we’ll dive deep into the ins and outs of Plan G, and its coverage benefits. You’ll learn exactly what Medicare Plan G includes, and how it compares to other popular Medicare supplement plans in 2024.

So sit back, relax, and let us guide you through the maze of Medicare Supplement Plan G.

Short Summary

- Medicare Supplement Plan G is a comprehensive insurance policy designed to work alongside Original Medicare, offering flexibility, and reducing out-of-pocket expenses.

- Eligibility requirements for Plan G include being an American citizen or legal resident, qualifying for Original Medicare, and enrolled in Medicare Part A & Medicare B.

- Benefits of this plan include hospital/skilled nursing facility care, doctor visits/outpatient services & foreign travel emergency coverage. It does not include dental/vision/hearing coverage or long-term care costs.

Understanding Medicare Supplement Plan G

Medicare Supplement Plan G, often referred to as Medigap Plan G, is a comprehensive insurance policy designed to work alongside Original Medicare (Parts A and B) to fill in coverage gaps and provide extensive benefits.

This popular plan, a type of Medicare Supplement Insurance, can help offset costs not covered by Original Medicare, potentially reducing out-of-pocket expenses for beneficiaries.

Unlike Medicare Advantage HMO plans, Medicare Supplement Plan G offers flexibility by being accepted wherever Medicare is accepted, providing a guarantee of renewal once enrolled.

How Plan G Works with Original Medicare

Medicare Plan G is designed to complement Original Medicare by covering most remaining costs after Medicare has paid its portion.

This includes co-pays, coinsurance, the Medicare Part A deductible, and even some additional expenses that Original Medicare does not cover. It’s important to note that the coinsurance responsibility for Medicare Plan G is 100% until the Medicare Part B deductible is met.

Insurance companies are responsible for selling Medicare Plan G policies, so it’s crucial to choose a reputable provider to ensure the best coverage possible.

In addition to covering the gaps in Original Medicare, Plan G also provides coverage for services that may not be included in Medicare Advantage or other Medicare plans, including Medicare-covered services.

This includes preventive care, emergency care, and care for chronic conditions. However, there are some services that Plan G does not cover, such as the Part B deductible, eye exams, and prescriptions. For these services, separate supplemental policies would need to be acquired.

Compare Medicare Plan G Rates in Your Area

Enter Zip Code

Eligibility requirements for Plan G

To be eligible for Medicare Supplement Plan G, individuals must meet the following criteria:

- Be American citizens or legal residents of the United States with at least five years of residency.

- Qualify for Original Medicare

- Enroll in Medicare Part A and Medicare Part B

Recently qualified Medicare beneficiaries are eligible to enroll in Medicare Plan G as well as other options that are close in benefits such as Medicare Supplement Plan N.

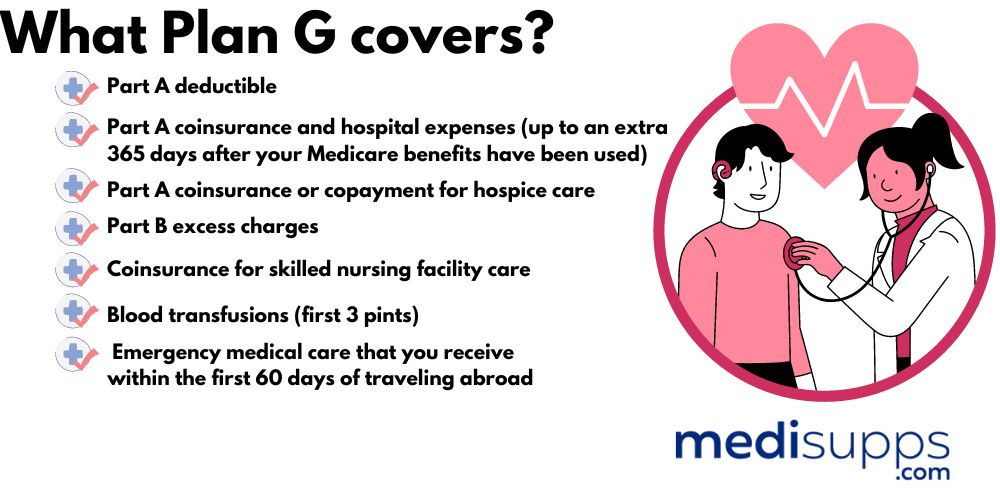

Comprehensive Coverage of Plan G

Plan G offers extensive coverage benefits that cater to a wide range of healthcare needs. Some of the benefits include:

- Hospital and skilled nursing facility care

- Doctor visits

- Outpatient services

- Foreign travel emergency benefits

With Plan G, your medical needs are taken care of, even when you’re exploring the world.

Let’s delve deeper into the specifics of Plan G’s comprehensive coverage.

Hospital and skilled nursing facility care

One of the essential components of Plan G’s comprehensive coverage is its provisions for hospital and skilled nursing facility care.

One of the essential components of Plan G’s comprehensive coverage is its provisions for hospital and skilled nursing facility care.

This includes coverage for the Medicare Part A deductible, which is the amount you must pay for hospital services before Medicare starts providing coverage. With Plan G, the Part A deductible is covered, ensuring that you don’t have to worry about out-of-pocket expenses for hospital stays.

In addition to covering the Part A deductible, Plan G also covers coinsurance for hospital and skilled nursing facility care.

This means that once you’ve met the deductible, Plan G will cover the remaining costs for hospital services, up to an additional 365 days beyond your standard Medicare benefit period.

This added peace of mind allows you to focus on your health and recovery, knowing that your medical expenses are well taken care of.

Doctor visits and outpatient services

![]() When it comes to doctor visits and outpatient services, Plan G has got you covered as well.

When it comes to doctor visits and outpatient services, Plan G has got you covered as well.

It covers Medicare Part B coinsurance, which means that after you’ve met the Part B deductible, Plan G will cover any additional medical expenses approved by Medicare for the remainder of the year.

However, it’s important to note that Plan G does not cover the Part B deductible itself.

Another key benefit of Plan G is its coverage of Part B excess charges, which refers to the amount a doctor may charge up to 15% more than the Medicare-approved amount for services or procedures.

This can be especially helpful if you frequently visit doctors who charge excess fees, as Plan G covers these additional costs, ensuring that you don’t face unexpected out-of-pocket expenses.

Foreign travel emergency benefits

Traveling abroad should be a time of adventure and discovery, but unexpected medical emergencies can happen.

Traveling abroad should be a time of adventure and discovery, but unexpected medical emergencies can happen.

Fortunately, Medicare Plan G offers foreign travel emergency benefits, providing coverage for emergency medical care during your international trips.

With this additional benefit, you can enjoy your travels with the assurance that you’ll have coverage for emergency medical needs outside of the country.

This coverage with Plan G offers a $50,000 lifetime maximum benefit and has a $250 deductible.

Comparing Plan G to Other Medicare Supplements

Given the wide range of Medicare Supplement plans available, it’s essential to compare Plan G to other popular options, such as Plan F and Plan N, to determine which plan best suits your needs and budget.

By understanding the differences and similarities between these plans, you can make an informed decision about the right Medigap plan for you.

Plan G vs. Plan F

One of the most popular Medigap plans, Plan F, is often compared to Plan G due to their similar coverage offerings.

The primary distinction between these two plans lies in the coverage of the Part B deductible. Plan F covers the Medicare Part B deductible, while Plan G does not. This means that with Plan G, you’ll need to pay the Part B deductible out-of-pocket before your coverage kicks in.

It’s important to note that as of January 2020, Plan F is no longer available to newly eligible Medicare beneficiaries.

If you’re considering enrolling in a Medicare Supplement plan and are not already enrolled in Plan F, you won’t have the option to choose Plan F moving forward.

In this case, Plan G may be the best choice for comprehensive coverage, with the only difference being the Part B deductible.

Medicare Plan G vs. Plan N

Another popular Medigap plan to consider is Plan N. While Plan G and Plan N share several common features, such as coverage for Medicare Parts A and B deductibles and coinsurance, skilled nursing and rehabilitation facility care, and foreign travel emergency coverage, there are some key differences between the two.

The primary distinction between Plan G and Plan N is the coverage for the Part B deductible and Part B excess charges. Plan G covers the Part B deductible and excess charges, whereas Plan N does not.

When comparing Plan G and Plan N, it’s important to consider the potential trade-offs. Plan G offers more comprehensive coverage, which results in higher monthly premiums.

On the other hand, Plan N has lower premiums but may involve more out-of-pocket costs due to the lack of coverage copays and possible excess charges.

Ultimately, the decision depends on your specific healthcare needs and financial preferences.

Costs and Premiums of Medicare Supplement Plan G

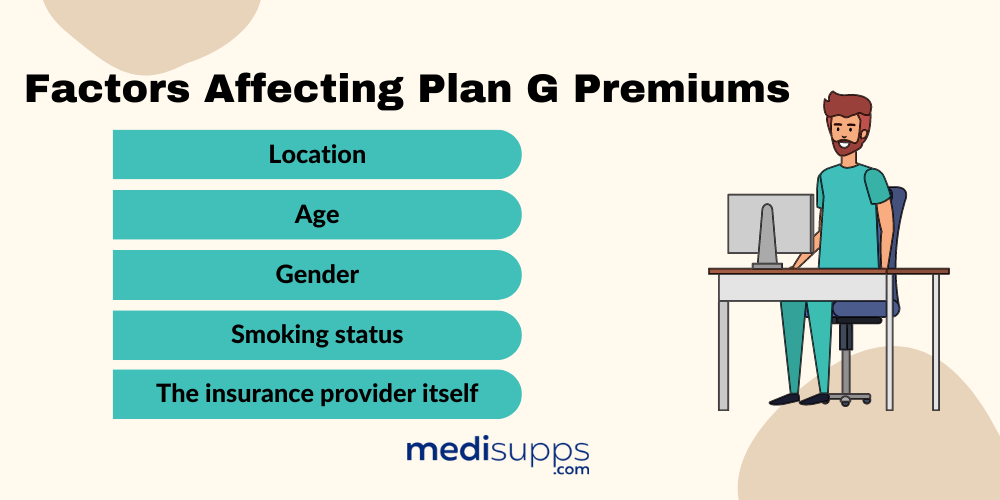

While Plan G offers comprehensive coverage and peace of mind, it’s important to consider the costs and premiums associated with this plan. Factors such as:

- Location

- Age

- Gender

- Tobacco use

- Household discounts if applicable

Can all impact the monthly premiums for Plan G, making it crucial to understand how these factors can affect your costs.

Let’s delve deeper into the factors that influence Plan G premiums and the high-deductible Plan G option.

Factors affecting Plan G premiums

Many factors can influence the premiums of Medicare Supplement Plan G, including:

- Location

- Age

- Gender

- Smoking status

- The insurance provider itself

Geographical location can play a role in Plan G premiums, as insurance companies may charge different rates in different states.

Age also impacts Plan G premiums, with insurance companies potentially charging higher rates for older individuals.

Gender and smoking status can further influence Plan G premiums, as insurance companies may charge different rates for male and female individuals, as well as higher rates for smokers.

Lastly, the insurance provider you choose can impact your Plan G premiums, as different insurance companies may have varying rates.

It’s important to research and compare various providers to find the best fit for your needs and budget.

High-deductible Plan G option

For those looking to lower their monthly premiums while still benefiting from the comprehensive coverage offered by Plan G, the high-deductible Plan G option might be the solution.

This option provides the same benefits as Plan G but requires meeting a higher deductible before coverage begins.

By choosing the high-deductible Plan G option, you can enjoy lower monthly premiums while still having access to the extensive coverage offered by Plan G.

Enrollment and Purchasing Medicare Supplement Plan G

Enrolling in Medicare Supplement Plan G may seem daunting, but understanding the best time to enroll and the process of purchasing a plan from a private insurance company can make the journey a breeze.

In this section, we will discuss the importance of enrolling during the Medigap Open Enrollment Period and provide guidance on choosing the right insurance company for your Plan G coverage.

The Medigap Open Enrollment Period is a six-month period that begins on the first day of enrollment into Medicare Part B.

The best time to enroll

The ideal time to enroll in Medicare Supplement Plan G is during the Medigap Open Enrollment Period, which starts when you turn 65 or become eligible for Medicare.

During the OEP, you can enroll in any Medigap plan without having to answer health questions or provide medical records, ensuring a seamless enrollment process regardless of your health status.

If you miss the enrollment period, you may still apply for a Medigap plan at any time during the year, just expect to have to answer medical questions and the possibility of denial due to medical underwriting.

All insurance companies have different underwriting guidelines and there are many options available, so give us a call today to see what you might qualify for.

Choosing an insurance company

When it comes to purchasing Medicare Supplement Plan G, selecting the right insurance company is crucial. Medicare Plan G can be purchased from private insurance companies such as Aetna, Allstate, Mutual of Omaha, and many more.

To choose the best provider for your needs, consider factors such as coverage requirements, financial constraints, and whether the insurance company offers any discounts.

Additionally, compare various providers in terms of pricing, industry ratings, customer service, and other relevant aspects to make an informed decision.

We can help you compare companies and rates in your area to find a plan that fits your needs best.

Services not covered by Medicare Plan G

While Plan G offers comprehensive coverage for many healthcare needs, there are some services that are not covered by this plan. These include:

- Dental

- Vision

- Hearing

- Long-term care

- Prescription drugs

To obtain coverage for these services, separate supplemental policies may be required.

It’s crucial to understand the limitations of Medicare Plan G coverage, as these services may represent significant out-of-pocket expenses if not properly accounted for.

By being aware of these limitations and seeking additional coverage where necessary, you can ensure that all of your healthcare needs are met and avoid unexpected financial burdens.

Summary

In conclusion, Medicare Supplement Plan G offers comprehensive coverage that fills the gaps in Original Medicare, providing beneficiaries with peace of mind and financial stability.

With coverage for hospital and skilled nursing facility care, doctor visits, outpatient services, and foreign travel emergencies, Plan G is a reliable and popular choice among Medicare recipients.

Understanding the costs, enrollment process, and limitations associated with Plan G is crucial for making an informed decision about your healthcare coverage.

Armed with this knowledge, you can confidently navigate the world of Medicare supplements and choose the plan that best suits your needs.

Get Quotes in 2 Easy Steps!

Enter Zip Code

Frequently Asked Questions

What does the Plan G cover?

Medicare Supplement Plan G covers coinsurance, copayments, and the deductible not covered by Medicare Part A. Other coverage includes hospital inpatient costs, skilled nursing facility care, hospice care, Part B coinsurance/copays, and the first three pints of blood if needed for a procedure.

These costs are typically not covered by Original Medicare, so having a Medicare Supplement Plan G can help you save money and provide peace of mind.

What does Plan G not cover?

Plan G does not cover the Medicare Part B deductible, dental care, vision care, hearing services, private-duty nursing, or prescriptions, so separate policies need to be purchased to provide coverage for these services.

We can help find the right coverage to fit your needs.

Is Medicare Plan G any good?

Medicare Plan G offers comprehensive coverage, providing a high level of peace of mind for new Medicare beneficiaries, and is the most comprehensive Medigap plan available for people new to Medicare. It covers almost all costs other than the Medicare Part B deductible, which is relatively low at only $226 in 2023. The deductible for 2025 should be close to this.

Thus, it can be concluded that Medicare Plan G is an excellent option.

What is the maximum out-of-pocket for Medicare Plan G?

Medicare Plan G has a maximum out-of-pocket cost of the Medicare Part B deductible ($226 for 2023). It covers all inpatient and outpatient expenses not paid for by Medicare, except for the annual Part B deductible.

This means that once you have paid the Part B deductible, you will not have to pay any additional out-of-pocket costs for the rest of the year. This makes Plan G a great option.

What is the main difference between Medicare Supplement Plan G and Plan F?

Medigap Plan F covers the Medicare Part B deductible, whereas Plan G does not, making this the main difference between the two plans.

Find the Right Medicare Plan for You

Finding the right Medicare Plan 2024 doesn’t have to be confusing. Whether it’s a Medigap plan, or you have questions about the Medicare Plan G, we can help.

Call us today at 1-888-891-0229 and one of our knowledgeable, licensed insurance agents will be happy to assist you!

Russell Noga is the CEO and Medicare editor of Medisupps.com. His 15 years of experience in the Medicare insurance market includes being a licensed Medicare insurance broker in all 50 states. He is frequently featured as a featured as a keynote Medicare event speaker, has authored hundreds of Medicare content pages, and hosts the very popular Medisupps.com Medicare Youtube channel. His expertise includes Medicare, Medigap insurance, Medicare Advantage plans, and Medicare Part D.