For years Medicare Supplement Plan F was the most popular choice for Medigap coverage because it provides 100% of the coverage gaps in Medicare Part A & B.

With Plan F you may visit any Dr., specialist, or hospital anywhere in the country that accepts Part B Medicare. Once you are there you will show your Medicare card and your Plan F card, and all approved expenses will be paid for you 100%.

With Plan F you may visit any Dr., specialist, or hospital anywhere in the country that accepts Part B Medicare. Once you are there you will show your Medicare card and your Plan F card, and all approved expenses will be paid for you 100%.

Medicare supplement plan F pays for items such as:

- Hospital Part A deductible

- Part B annual deductible

- 20% of Medicare Part B coinsurance

- Hospital coinsurance

- Skilled nursing facility coverage

What is Medicare Supplement Plan F?

As of January 1st of 2020, Plan F became a “closed block of business” for any new beneficiaries of  Medicare. Simply put, if you were eligible for Medicare on January 1st of 2020 or later, you may not enroll in a Plan F.

Medicare. Simply put, if you were eligible for Medicare on January 1st of 2020 or later, you may not enroll in a Plan F.

Medicare has removed this plan from the lineup for all new people entering the Medicare system as it was too expensive.

Those who were enrolled in Medicare prior to that date may keep their plan F if they have one, or they may still switch to a Plan F from a different plan.

We do NOT recommend this! Plan F is now experiencing the highest rate increases of any plan and we didn’t recommend Plan F prior to it being removed.

Medicare Plan F

Plan F is offered by private insurance companies and the benefits are standardized by Medicare. This means that regardless of which company offers a Medicare supplement plan F the benefits must be identical.

What makes it interesting is the fact that all companies have different premiums for exactly the same coverage.

Medicare Supplement Plan F offers the most benefits of all the options, often called Medigap Plan F, it provides coverage for Part A and Part B deductibles, coinsurance, and copays.

Beneficiaries have zero out-of-pocket expenses for any Medicare-approved service.

For years, most seniors have enrolled in Plan F coverage, making it a popular choice. Professionals with America’s Health Insurance estimate 57% of policies have been Plan F.

At the same time, Medicare Plan G is the most popular alternative option over Plan F.

Medicare Supplement is designed to help cover the out-of-pocket costs left after Medicare pays 80%. This includes coinsurance, copays, and deductibles.

Medicare Supplement is designed to help cover the out-of-pocket costs left after Medicare pays 80%. This includes coinsurance, copays, and deductibles.

They are not a replacement for Medicare Part B, and you are required to have Part A and B before enrolling with a Medicare Supplement.

After purchasing Plan G or Plan F with your Traditional Medicare, coverage becomes very comprehensive. Plan F offers the most benefits, which is the correct terminology. Although, it is often referred to as Medigap Part F or Medicare Part F.

100% Coverage

Seniors prefer Plan F over the others due to it covering all the out-of-pocket expenses that Medicare doesn’t cover. This includes outpatient and hospitalization, Part B deductible, and the 20% copay, The only thing Medicare Supplement Plan F does not cover, is prescription drug coverage.

You will have NO out-of-pocket costs for doctor visits, ever.

Therefore, it’s simple to answer the frequently asked question: Which plan is best?

Get Comprehensive Coverage with Medicare Supplement Plan F

The term “first dollar coverage” refers to plans that pay the remaining balance after Medicare pays their part without the enrollee paying any out of pocket costs.

The following are the benefits of Plan F:

- It will fully cover deductibles for Part A hospitalizations and Part B outpatient services

- It will cover the 20% Part B copay

- Select any doctor in the U.S.

- All excess charges from Part B are covered, eliminating the stress of paying up to 15% more per visit

- Guaranteed renewal without cancelation from the number of claims or health conditions

- No referral is needed from a primary care physician to see a specialist

It is obvious that Medicare Supplement Plan F is the most comprehensive coverage and offers the most worry-free benefits, except for the high cost.

The best part is, no matter which insurance company you prefer, all Plan F policies must cover these benefits.

Medicare “Gaps”

The following is an example of how much Plan F can save you.

In 2020, the deductible for Part A is $1,408. You would owe this before Medicare Part A kicks in.

Additionally, Part B only covers 80% of costs, leaving 20% out-of-pocket expenses. Therefore, a $10,000 claim would end up costing $3,308 out of pocket.

With a Plan F policy, all these expenses are covered. It is recommended that you compare rates between companies because there are many smaller name companies that offer lower rates compared to big brands.

Just remember to review their ratings.

There are free Medicare webinars available that offer additional information to those new to Medicare Supplement plans too. These can help you determine which options are best for you.

Medicare Supplement Plan F Cost

The overall cost of Plan F premiums depends on many factors, including your location, gender, if you smoke, and many others.

The average rates tend to range from $120 to $140 per month for a female that recently turned 65. Of course, to get an accurate quote, it’s recommended that you get several quotes.

On average, rates are a little higher for males. In addition, smokers frequently have a higher premium compare to those that do not.

On average, rates are a little higher for males. In addition, smokers frequently have a higher premium compare to those that do not.

Finally, some insurers offer household discounts if multiple people have a plan, such as a spouse.

Sometimes people are scared to change insurance carriers because they’ve had Plan F for years, and they are scared of losing coverage.

The positive part is, Medicare Supplement Plan F will provide the same coverage no matter the insurance company it’s with. Instead, the annual rate should be compared between carriers to find the best price.

You can save by comparing rates and getting quotes each year.

Most States Require Underwriting When Changing

Remember, after your initial six-month open enrollment period expires, you will typically be asked a  series of health-related questions when applying for Medicare Supplement Plan F or others.

series of health-related questions when applying for Medicare Supplement Plan F or others.

About 3 out of 4 of our customers pass the underwriting process without any issues.

By using a service like ours that compares the rates of Plan F policies annually, you can ensure you are up to date on the best deal for your area.

Our system is designed to quickly compare rates between companies and compare against other Medicare Plans too.

We also offer to review your answers to health questions. This allows us to determine if you’re likely to pass the underwriting process and get a lower rate.

A big debate about what the best Medigap Plan is is Medicare Plan F vs Plan G.

Medicare Plan F vs G

Another common question is, Plan G vs. Plan F, which is the better option? Most of our customers compare the rates between these two plans because the only difference is the Part B deductible not being included under Plan G for a cheaper premium.

In 2024, this deducible is $240. And in 2025 it will be $257.

We often find that Plan G can average up to $300 less annually compared to Plan F. So, which is the better deal, and why?

We often find that Plan G can average up to $300 less annually compared to Plan F. So, which is the better deal, and why?

As you can see, the coverage is very similar to each other. The only exception being the deductible for Medicare Part B.

While you’ll have an annual out-of-pocket expense for the initial service(s), premiums can be lower, saving you each month.

By opting for Medicare Supplement Plan G, you could put the savings towards savings or a Medicare Part D drug plan. If needed, you may reach out to us, and we can help you with quotes between Plan F, Plan G, and Plan N.

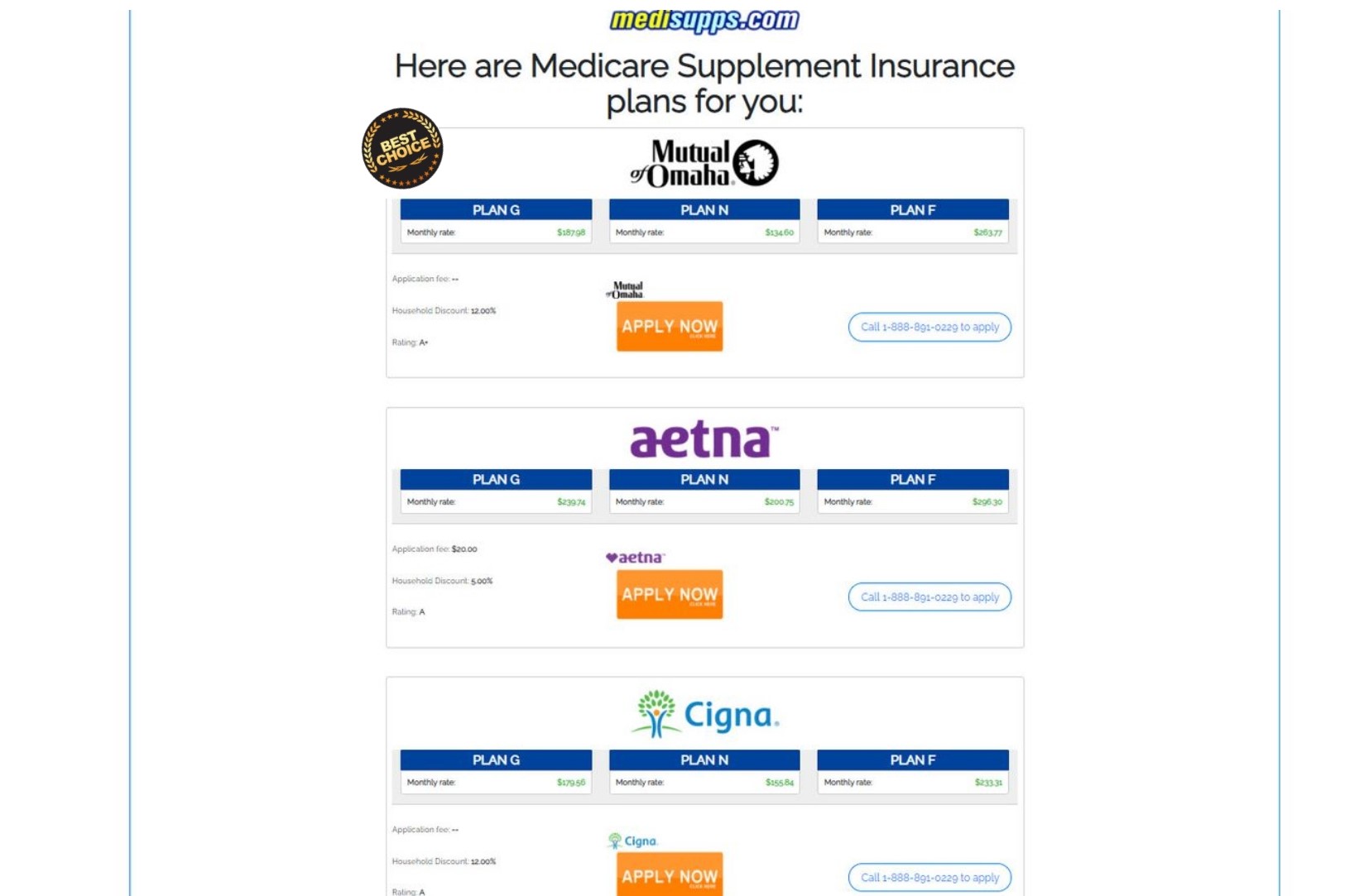

We are partnered with around 30 insurance companies in each state to help offer you the best rates. Carriers include Aetna, Mutual of Omaha, Allstate, and many more that offer Plan G policies for 2025.

Using a comparison tool is a fast way to learn about the best benefits and long-term savings between plans.

FAQ’s About Medicare Supplement Plan F

- What’s the difference in Medicare Plan F and Part F?

There are four parts to Traditional Medicare, Part A, Part B, Part C, and Part D. However, there are up to ten plans for Medicare Supplement, which would be correctly stated as Plan ‘Letter’, such as Plan F.

The easiest way to remember the difference is, Medicare Supplement offers Plans, while Medicare offers Parts.

- Is Plan F Still Available?

If you were enrolled in Medicare before January 1, 2020, then you are still allowed to purchase it.

- What’s Covered By Medicare Supplement Plan F?

All of the services covered by Medicare Part A and Part B are covered, including the gaps or expenses that are not covered.

- Are Prescriptions Covered by Plan F?

Medicare Supplement plans will all cover medications given in a clinic or hospital environment. But, they do not cover prescribed medications you must get from a pharmacy. To have drug coverage, you will need a Medicare Part D policy.

- Will Plan F Cover Hearing, Vision, or Dental?

No, Medicare Supplement plans do not cover these services or routine checkups. If you would like coverage for these, there are individual plans that offer hearing, vision, and dental coverage at a reasonable rate.

- Will a Plan F Policy Cover Chiropractic Care?

Yes, because chiropractic care is covered under Medicare. Medicare will cover 80%, and then Medicare Supplement Plan F will cover the remaining 20% of services, including x-rays.

- What is the Most Common Plan?

In 2020, the most popular Medicare Supplement Plan G. For years, Plan F has been the ultimate option, but due to the phasing out of Plan F, the second most popular option is quickly becoming Plan G.

Even if you qualify for Plan F, you should get a quote for both plans to determine which offers the best savings.

- What are the Top Insurance Companies in 2025?

The best insurance company in your area may be different than the best in another.

However, because the Medicare Supplement plans are required to offer the same benefits between companies, you do not have to worry about that part.

You should compare different plans to determine the lowest rate for you.

The rates are often determined by many factors, such as your state, area, gender, age, and tobacco usage. Some companies offer household discounts too.

Is Medicare Supplement Plan G Better Than F?

The answer is a little more complicated than yes or no. Yes, Plan F offers more benefits by covering Part B deductibles.

However, Plan G offers a lower monthly premium, which could save more annually. Because they are just starting to phase out Plan F, many that already had it will continue receiving the full benefits.

Those who qualified before 2020 can still be accepted for Plan F if they pass the underwriting questions.

Therefore, if you still qualify for Plan F, it’s still considered the best option available. Many questions if they should still enroll in a plan that’s being phased out, or if Plan G is the better long-term option.

Some agents may try talking people into switching to Plan G with the new changes in 2020, referred to as scare tactics. However, you should not panic if you’ve already got Plan F or if you would pass the underwriting process.

In the end, you should make a choice based on what is best for your financial situation.

That is why we recommend getting quotes for both plans to determine if the lower Plan G premium will outweigh the Part B deductible, which is $240 in 2024.

Many of our clients have found Plan G to be the better option, simply because of the annual savings. For example, they may save $300/year on premiums compared to Plan F.

Medicare Supplement Plan F Review

We have to give Medicare Supplement Plan F a 5-star rating because it offers the most comprehensive  coverage of them all. Unlike the other plans, we find Plan F benefits to be the easiest to understand.

coverage of them all. Unlike the other plans, we find Plan F benefits to be the easiest to understand.

You pay your monthly premium, and all Medicare-approved services are covered without any out-of-pocket expenses.

Because of the easy math, we often find Plan F to be the simplest starting point for receiving quotes. Of course, we always suggest getting quotes for Plan G alongside them.

If Medicare is something you’re just learning about, start with learning how Traditional Medicare works. From there, it gets easier to understand the Medicare Supplement Plan benefits.

We offer free support to our customers. If your claim is denied by Medicare due to miscoding by the doctor or another issue, we’re here to help you get it corrected. You may reach out to us at 1-888-891-0229.

When To Enroll in Plan F

Anyone turning age 65 and enrolled in Part B Medicare has a six-month open enrollment period to obtain any Medicare supplement plan without medical underwriting.

This means that regardless of pre-existing conditions everyone will be approved for a plan.

If you currently already have a Medigap plan you can switch plans at any time during the year. You do not have to wait until October to change plans!

For those of you who still have Plan F, call us today! There’s no need to wait to switch and start saving money.

Russell Noga is the CEO and Medicare editor of Medisupps.com. His 15 years of experience in the Medicare insurance market includes being a licensed Medicare insurance broker in all 50 states. He is frequently featured as a featured as a keynote Medicare event speaker, has authored hundreds of Medicare content pages, and hosts the very popular Medisupps.com Medicare Youtube channel. His expertise includes Medicare, Medigap insurance, Medicare Advantage plans, and Medicare Part D.