by Russell Noga | Updated November 13th, 2023

Medicare supplement plans (Medigap) were designed along with Medicare to help people pay the gaps, or expenses that Medicare Part A and Part B do not pay.

These “gaps” include items such as:

- Deductibles

- Coinsurance

- Co-pays

Unlike the parts of Medicare such as Part A, B, and D, Medicare supplements are “plans”, and are designated by plan letters that run A – N. Many people stick to popular Medigap Plans such as Plan F, G, and N due to the outstanding coverage and relatively low premiums.

Medigap Plan L and K offer lower benefits and typically are not worth the cost in many areas.

These plans are offered by private insurance companies, and the benefits of each plan are standardized by Medicare. This means that regardless of which company you obtain your plan from, they all must offer the same benefits within each plan letter.

For example, Mutual of Omaha Medicare Supplement plans and letters are all identical to Aetna Medicare Supplement Plans.

Medicare supplement plans help pay for the gaps in Medicare Part A (hospital coverage) and Medicare Part B (doctor’s services) and do not include Medicare Part D prescription drug coverage.

Medicare Supplement Plans have NO Network

While many Medicare Advantage plans do offer prescription drug coverage within their plans, that does not necessarily mean they are better coverage.

For example, with a Medicare Advantage plan, you are typically required to remain in your network to get coverage. Medicare supplement plans have no network. You may visit any doctor, specialist, or hospital in the country and use your coverage provided they simply accept Medicare Part B.

With the ability to choose your own doctor and never need a referral or prior authorization for any Medicare-approved services, Medicare supplement plans outshine advantage plans when it comes to the best coverage in many areas of the country.

We can help show you all the options available in your area both to help you decide which would work best for you.

View Rates in 2 Easy Steps

Enter Zip Code

Medicare Supplement Plan Enrollment Periods

For most people, the best time to enroll in a Medicare supplement plan is during the 6-month Medigap open enrollment period. This period begins the day your Medicare Part B goes into effect and lasts 6 months. During this time you may apply for any Medicare supplement plan and be guaranteed coverage regardless of any medical conditions. You may apply up to 6 months prior to your effective date for a Medicare supplement with most companies.

Turning 65?

For anyone who is just turning age 65 and first eligible for Medicare, you have the option of enrolling in any Medicare supplement plan that you choose and you cannot be turned down for coverage.

This period lasts six months from the effective date of your Part B Medicare. Anyone with pre-existing conditions should absolutely take advantage of this time frame in case you have trouble getting approved down the road.

Once this six-month period is over will have to go through medical underwriting if you wish to enroll in or change your Medicare supplement policy.

Coming off Employer Health Coverage?

If you’re over the age of 65 and still working and receiving medical benefits from your employer, then you could be eligible to enroll in a Medicare supplement policy regardless of any health conditions.

This means you have opted out of Medicare Part B and are retiring and first enrolling in Part B. We can help find you the right Medicare supplement plan and apply for coverage, and you will not need to answer any medical questions. During this time you may choose any of the Medicare supplement plans to enroll in and you are guaranteed coverage.

Medicare Supplement Plans are Guaranteed Renewable

Regardless of which supplement plan you enroll in the policy is guaranteed renewable each month. This means that as long as you pay your monthly premium on time an insurance company can never terminate your policy.

Your policy can never be terminated for your own health claims, and future rate increases for your monthly premium are also not determined by the amount of your own personal claims.

Compare 2024 Plans & Rates

Enter Zip Code

Compare Medicare Supplement Plans

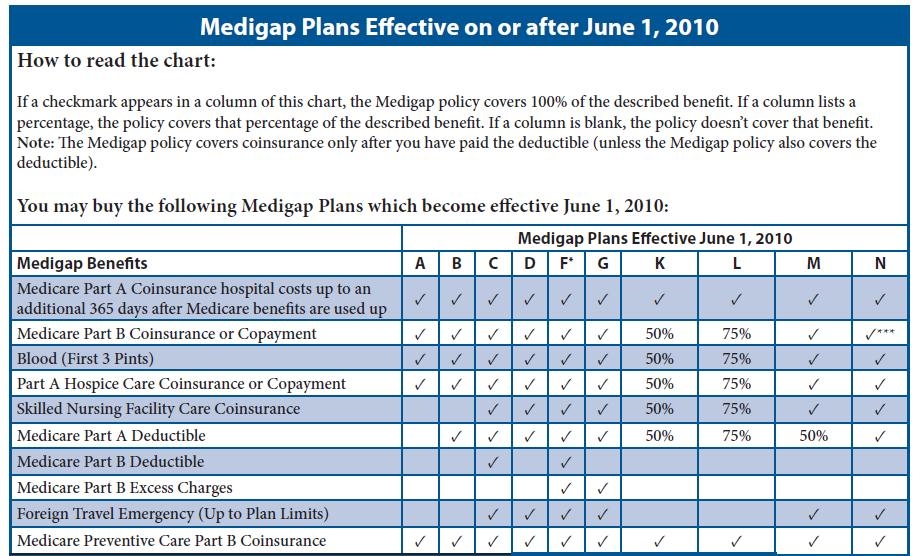

Insurance companies offer Medicare supplement plans that are lettered A – N. There are twelve plans to choose from that are offered by private insurance companies.

These plans are standardized by the government, which means they all must offer identical coverage regardless of which company offers them. The rates from each company, however, are entirely different! This means a Medicare Plan G offered by one company could be much more expensive than what another company is charging.

How do you choose?

The best way to shop for Medicare supplement plans in 2024 is to allow us to help. We are independent brokers, and for no charge, at all, we help provide you with a comparison of the lowest premiums for your Medigap coverage as well as your Medicare Part D drug plan. By shopping all the top companies each year, we’ll make sure you don’t overpay for your coverage.

And with 2024 just around the corner, it’s smart to start shopping now for the best plans.

View the Medicare Supplement plans comparison chart below to view the different plans available.

The Best Medicare Supplement Plans

There are currently 10 different Medicare supplement plans available, however, there isn’t one “best Medicare supplement plan” for everyone. That being said, there really are just a few plans that most people end up enrolling in.

The most popular Medicare Supplement Plans are:

- Medicare Plan G

- Medicare Plan N

- Medicare High-deductible Plan G

- Medicare Plan F*

* Medicare Plan F is not available to anyone enrolled in Medicare Part A on January 1st, 2020, or later

Medicare Supplement Plans for 2024

The most popular Medicare Supplement plans for 2024 are

- Medicare Plan G

- Medicare Plan N

- High-deductible Plan G

- Medicare Plan F

Medicare Supplement Plan G in 2024

Medicare Plan G is currently the most popular Medicare supplement plan available due to its fantastic coverage and relatively low premiums. For anyone enrolling in Medicare on January 1st of 2020 or later, Medicare Plan G is the most comprehensive Medigap plan they can possibly enroll in.

Medicare Plan G Benefits

Medicare supplement plans are just that, they supplement the coverage of Medicare Part A and B. Medicare Part B (doctor’s services) does not begin paying anything until you first pay a deductible once per year. This is a specific amount of your medical bills that you must first pay, prior to Medicare paying. This is called the annual Part B deductible, and this amount changes each year. In 2025, this deductible amount is $257.

With Medicare Supplement Plan G, this annual Part B deductible is the only expense that you are required to pay prior to both Medicare and Plan G paying 100% of your medical costs.

For example, let’s say on January 1st, 2022 you visit your doctor and the bill is $300. Prior to Medicare paying anything, you’re required to pay the first $257 (the annual Part B deductible). So you’ll get a bill for the $257, and after that Medicare and Plan G will pay 100% of your medical bills for the rest of the calendar year.

Medicare Plan G Cost

As previously mentioned, the cost for a Medicare supplement plan will vary from company to company so it’s important to let us help you shop the rates. These rates are not easily available for the average consumer to obtain. A quick and easy way to check rates is to click the button in the upper right-hand corner of our site to compare plans and rates right here on this website. We actually do show you the rates, and we do not sell your information.

Medicare Plan G’s cost can vary anywhere from $85 per month up to over $200 depending on age and which part of the country you live in.

Medicare supplement rates are determined by various factors. These include:

- Gender

- Age

- Zip Code

- Tobacco use

- Household discounts if applicable

Medicare Supplement Plan N 2024

Medicare Plan N is becoming increasingly popular due to its lower premiums than Plan G. In exchange for lower premiums, there are a few additional out-of-pocket expenses that could occur.

With Plan N you still pay the annual Part B deductible just as you do with Plan G. The difference between the two plans, aside from the fact that Plan N has lower monthly premiums, is on Plan N after you pay the annual Part B deductible, you might have up to a $20.00 co-pay per doctor’s visit. This only applies to in-person visits and not telehealth visits.

As well, with Plan N if you visit the emergency room and you are not admitted, you will have to pay a $50 co-pay. This does not apply to urgent care facility visits though.

Medicare Part B Excess Charges

One more out-of-pocket expense that could come up with Plan N, is called Part B excess charges. These are charges that could come up only if your doctor does not accept what is called “Medicare assignment”. Approximately 99% of doctors in the country do accept the assigned rates from Medicare and will not charge Part B excess charges.

In the event your doctor does not accept assignment, they can charge up to 15% extra of what Medicare would normally charge, and they must do this for their entire practice.

The following states are not even allowed to charge Part B excess charges. If you live in one of these states you should absolutely let us help you compare rates for Medicare Plan N:

- CT

- MN

- OH

- PA

- RI

- VT

- MA

- NY

Medicare Plan N vs Plan G

With Medicare Plan N vs Plan G being the two most popular plans, how do you choose which is best for you?

For people who want as few medical expenses as possible and don’t mind paying a little extra for that, then Medicare Plan G is likely the better choice. With just one small deductible to pay, Plan G offers the most coverage.

If you are open to the possibility of getting a few co-pays for doctor’s visits, or perhaps you’re in very good health but you still want great coverage, then Medicare Plan N is a fantastic option. We are now switching more people than ever to Plan N due to its nice low premiums each month, as well as lower rate increases than Plan G.

Lower Monthly Premiums

Medicare Plan N has lower monthly premiums than Plan G. In fact, depending on the area and your age, Plan N can be up to $30 less per month than Plan G. That means that even if you visit your doctor 6 times per year and you have to pay the full co-pay of $20 each time, you’ll save a good amount of money on Plan N.

For those who visit the doctor more often, Medicare Plan G might be the better option so you can avoid any co-pays per doctor’s visit.

Let us help compare the difference in premiums on both to make sure you end up with the right plan for you.

View Rates In Your Area

Enter Zip Code

Medicare Supplement Plan F

Medicare Plan F was the most popular Medigap plan for years because it paid 100% of the gaps in Medicare Part A and B. This became extremely expensive for everyone, and for that reason, Plan F is no longer available for people new to Medicare to enroll in. The only people who are eligible to have Plan F are those who were enrolled in Medicare prior to January 1st of 2020.

While Plan F pays 100% of the gaps in Medicare, you will also pay a higher premium for this. For many people, Medicare Plan G is a far better option. The only difference between Plan G and Plan F is who pays the annual Part B deductible. On Plan G, you must pay this deductible yourself. After that is met, Plan G pays 100% just like Plan F does. You’ll pay lower premiums though for Plan G, often much less than the deductible amount making Plan G a much better choice economically.

Regardless of which plan you choose it is extremely important to shop the rates from multiple companies before purchasing a policy.

As independent agents, we can easily do this for you in just a few minutes to make sure you pay the lowest premiums possible, whether you’re interested in a Medicare supplement plan and Part D drug plan, or a Medicare Advantage plan.

Call us direct at 888-891-0229 to begin today!

Medicare Supplement Plans by State

Companies

Russell Noga is the CEO and Medicare editor of Medisupps.com. His 15 years of experience in the Medicare insurance market includes being a licensed Medicare insurance broker in all 50 states. He is frequently featured as a featured as a keynote Medicare event speaker, has authored hundreds of Medicare content pages, and hosts the very popular Medisupps.com Medicare Youtube channel. His expertise includes Medicare, Medigap insurance, Medicare Advantage plans, and Medicare Part D.