by Russell Noga | Updated May 8th, 2023

What is Medigap?

Medigap, also known as Medicare Supplement Insurance, offers additional coverage to help fill the gaps in Original Medicare. These plans can provide financial relief for seniors by covering out-of-pocket costs such as Medicare deductibles, co-payments, and coinsurance.

This comprehensive guide will discuss what Medicare Supplement plans are, their coverage, the best options available, and how and when to enroll in a Medigap plan.

How Medigap Works

Navigating the world of health insurance can be challenging, especially when it comes to understanding the gaps in Medicare coverage and the changing nature of Medigap. Fortunately, Medicare Supplement Insurance, also known as Medigap, exists to bridge these gaps. But how does Medigap work? Let’s delve into it.

Medigap is private health insurance designed to supplement Original Medicare (Part A and Part B). Original Medicare covers a significant portion of healthcare costs, but it doesn’t cover everything.

Beneficiaries are often left with out-of-pocket expenses such as copayments, coinsurance, and deductibles. That’s where Medigap comes into play. It helps cover these additional costs, offering beneficiaries peace of mind and financial protection.

When you have a Medigap policy, Medicare pays its share of the Medicare-approved amounts for healthcare costs, and then your Medigap policy pays its share. Each Medigap policy must follow federal and state laws designed to protect beneficiaries, and it must be clearly identified as “Medicare Supplement Insurance.”

Medigap plans are standardized across most states, which means that each plan of the same letter (A through N) provides the same benefits regardless of the insurance company offering it. However, insurance companies can charge different premiums for the same coverage. This makes shopping around and comparing prices a crucial step when choosing a Medigap plan.

It’s important to note that Medigap plans do not include prescription drug coverage. If you need help with medication costs, you should consider enrolling in a separate Medicare Prescription Drug Plan (Part D).

Enrollment in a Medigap policy is best during your Medigap Open Enrollment Period, a six-month timeframe that begins the month you turn 65 and are enrolled in Medicare Part B. During this period, you have a guaranteed right to buy any Medigap policy sold in your state, regardless of health status.

What are Medigap Plans?

Medigap plans are supplemental insurance policies designed to cover the gaps not covered by Medicare Part A (hospital insurance) and Medicare Part B (medical insurance). Private insurance companies offer these policies to Medicare beneficiaries who want extra coverage beyond what is provided by Original Medicare.

It is important to note that Medigap plans do not cover prescription drugs; for this, you will need a separate Medicare Part D plan.

There are currently 10 Medigap plans available, with 2 additional high-deductible versions of Plan F and Plan G.

The most popular Medicare Supplement Plans are Medicare Plan F, Plan G, and Plan N.

What Do Medigap Plans Cover?

A Medigap plan can help cover out-of-pocket costs associated with Original Medicare, such as:

- Part A deductible

- Part B deductible

- Part A coinsurance for hospital stays

- Part B coinsurance or copayment

- Skilled nursing facility care coinsurance

- Part A hospice care coinsurance or copayment

- Blood (first three pints)

- Foreign travel emergency care (limited)

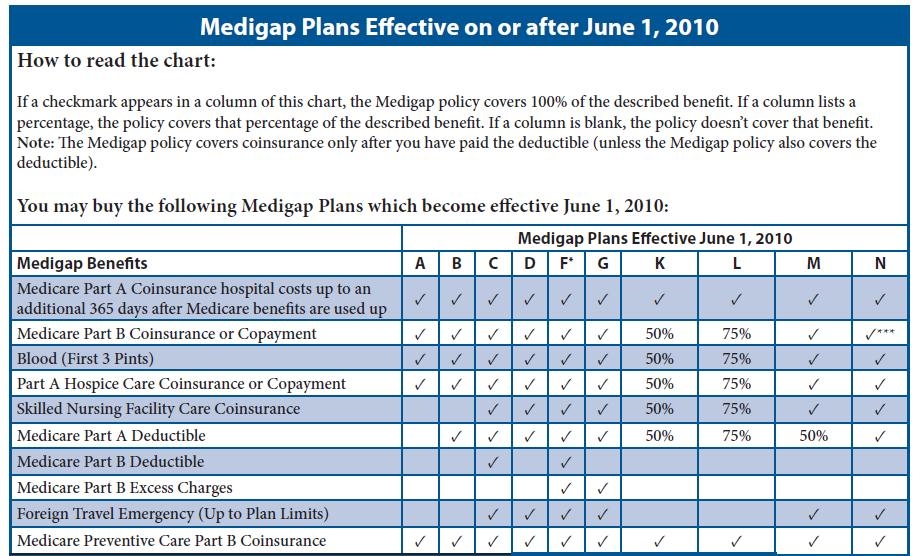

The level of coverage varies depending on the specific plan you choose. There are ten standardized supplement plans (A, B, C, D, F, G, K, L, M, and N) available in most states, each offering different levels of coverage.

When it comes to Medicare, there are many options available to help cover the gaps in coverage that the program may not provide. Medigap plans, also known as Medicare Supplement plans, are one such option.

If you’re considering a Medigap plan, it’s important to understand the various options available and how they compare to one another. In this article, we’ll explore the basics of Medicare Supplement Insurance plans and provide a comparison chart to help you make an informed decision.

How Many Medigap Plans are Available?

As mentioned above, there are ten standardized supplement plans available. These plans are labeled A, B, C, D, F, G, K, L, M, and N. Each plan offers different levels of coverage, and the benefits covered by each plan are standardized across all insurers. This means that Plan A from one insurer will offer the same Medicare Supplement coverage as Plan A from another insurer.

What is the Difference Between Medigap Plans and Medicare Advantage Plans?

Medicare Supplement Plans work with Original Medicare Part A and Medicare Part B and help supplement the costs of those. With a Medicare Advantage plan you opt out of Original Medicare and enroll with a private insurance company to receive your benefits. You may only enroll in one or the other, not both.

Compare Medicare Plans & Rates in Your Area

Medicare Supplement Insurance is Standardized

The benefits covered by each Medicare Supplement plan are standardized across all insurers by the federal Medicare Program. For example, this means that a Plan G from one insurer will offer the same coverage as Plan G from another. This makes it easier for consumers to compare Medicare Supplement insurance plans and select the one that best fits their needs.

Which Insurance Company is Best?

While the benefits covered by each plan are standardized, the premiums charged by insurers may vary. However, the way premiums are calculated is also standardized. Insurance companies can use one of three methods to determine premiums:

Community-rated: The same premium is charged to all policyholders, regardless of age.

Issue-age-rated: The premium is based on the age of the policyholder when the policy is issued. The younger the policyholder, the lower the premium.

Attained-age-rated: The premium is based on the policyholder’s current age, meaning that the premium will increase as the policyholder gets older.

Medigap Enrollment Period

There are specific enrollment periods during which beneficiaries can enroll in or switch plans without facing medical underwriting, which means that insurance companies cannot deny coverage or charge higher premiums based on pre-existing conditions. These enrollment periods include:

6-month Medigap Open Enrollment Period: This is the six-month period that begins on the first day of the month in which a beneficiary is both 65 or older and enrolled in Medicare Part B.

Open Enrollment Period: This is a one-time, six-month period that begins on the first day of the month in which a beneficiary is both 65 or older and enrolled in Medicare Part B. During this period, beneficiaries can enroll in any Medicare Supplement plan without having to go through medical underwriting.

Guaranteed Issue Period: This is a period during which beneficiaries have a guaranteed right to enroll in a Medicare supplement plan without facing medical underwriting. Guaranteed issue rights may arise when a beneficiary loses other health coverage, such as employer-sponsored coverage, or when an insurer discontinues a Medigap plan.

When to Enroll

There is no specific Medicare Supplement open enrollment period. If you are enrolled in Medicare and not a Medicare Advantage plan, you may apply for Medigap coverage at any time during the year.

The standardization of Medigap benefits, premiums, and enrollment periods makes it easier for consumers to understand and compare their options.

Medigap vs Medicare Advantage

When it comes to health coverage for seniors, Medicare offers several options. Two of the most popular choices are Medigap (also known as Medicare Supplement Insurance) and Medicare Advantage. Both options offer ways to cover healthcare costs beyond Original Medicare, but they differ significantly in costs, benefits, and structure. Here’s a comprehensive comparison of Medigap and Medicare Advantage to help you make an informed decision.

What is Medigap?

Medigap is private insurance that supplements Original Medicare (Parts A and B). It covers out-of-pocket costs like copayments, coinsurance, and deductibles, essentially filling the “gaps” in Medicare coverage. Medigap policies do not include prescription drug coverage, so beneficiaries often pair it with a standalone Medicare Part D plan.

Pros of Medigap:

- Broad Provider Network: Medigap allows you to see any doctor or specialist that accepts Medicare, without needing referrals or dealing with network restrictions.

- Predictable Costs: Medigap offers predictability in healthcare spending as it covers most, if not all, out-of-pocket costs that Original Medicare does not cover.

- Standardized Benefits: Medigap plans are standardized, making it easier to compare policies.

Cons of Medigap:

- Higher Monthly Premiums: Medigap plans typically have higher monthly premiums compared to Medicare Advantage plans.

- No Additional Benefits: Medigap policies only cover the gaps in Original Medicare. They do not offer additional benefits like vision, dental, or prescription drug coverage.

What is Medicare Advantage?

Medicare Advantage (Part C) is an all-in-one alternative to Original Medicare. These plans are offered by private insurance companies and combine Parts A and B and often Part D (prescription drug coverage). They may also offer additional benefits like dental, vision, and hearing care.

Pros of Medicare Advantage:

- Extra Benefits: In addition to providing all the benefits of Original Medicare, most Medicare Advantage plans also offer additional benefits like dental, vision, hearing, and wellness programs.

- All-in-One Coverage: With many plans including prescription drug coverage, Medicare Advantage offers a convenient, all-in-one solution.

Cons of Medicare Advantage:

- Provider Networks: Medicare Advantage plans often have network restrictions, which may limit your choice of doctors and hospitals.

- Potentially High Out-of-Pocket Costs: While many Medicare Advantage plans offer low or even $0 monthly premiums, they can have higher out-of-pocket costs when you need care.

Medigap vs. Medicare Advantage: The Bottom Line

The choice between Medigap and Medicare Advantage depends on your healthcare needs, budget, and preferred style of coverage. If you value broad access to providers and predictability in costs, Medigap might be a better fit. On the other hand, if you’re seeking lower monthly premiums and additional benefits, a Medicare Advantage plan may be more suitable.

Remember, there’s no one-size-fits-all solution. Take time to understand your healthcare needs and compare plan options to make the right choice for you.

Medicare Supplement Plans Comparison Chart

To help you understand the differences between Medicare Supplement insurance plans, we’ve created a comparison chart. This chart provides an overview of the benefits covered by each plan, along with any cost-sharing requirements.

Keep in mind that while the benefits covered by each plan are standardized, the premiums charged by insurers may vary.

Medicare Supplement Plans - An Overview

Medicare Supplement Plan A: This plan covers basic benefits, including Medicare Part A coinsurance and hospital costs, Medicare Part B coinsurance or copayment, and the first three pints of blood each year.

Medicare Supplement Plan B: In addition to the benefits covered by Plan A, Plan B also covers the Medicare Part A deductible.

Medicare Supplement Plan C: This plan offers comprehensive coverage, including coverage for skilled nursing facility care coinsurance, Medicare Part B deductible, and foreign travel emergency care.

Medicare Supplement Plan D: This plan offers coverage similar to Plan C but does not cover the Medicare Part B deductible.

Medicare Supplement Plan F: This plan offers the most comprehensive coverage, including coverage for the Medicare Part B deductible and excess charges. However, as mentioned earlier, Plan F is no longer available to new Medicare beneficiaries.

Medicare Supplement Plan G: This plan is similar to Plan F but does not cover the Medicare Part B deductible.

Medicare Supplement Plan K: This plan offers limited coverage, with the beneficiary paying a percentage of all covered benefits.

Medicare Supplement Plan L: This plan offers more coverage than Plan K, but the beneficiary is still responsible for a percentage of covered benefits.

Medicare Supplement Plan M: This plan offers comprehensive coverage, but the beneficiary pays 50% of the Medicare Part A deductible.

Medicare Supplement Plan N: This plan offers comprehensive coverage, but the beneficiary may be responsible for copayments of up to $20 for some doctor’s visits and up to $50 for emergency room visits that do not result in an inpatient admission.

What are the Best Medigap Plans?

The best supplement plan for you depends on your individual needs, budget, and preferences.

Despite there being ten plans available, there really are just a few plans that the majority of people on Medicare choose.

The Top Medicare Supplement Plans are:

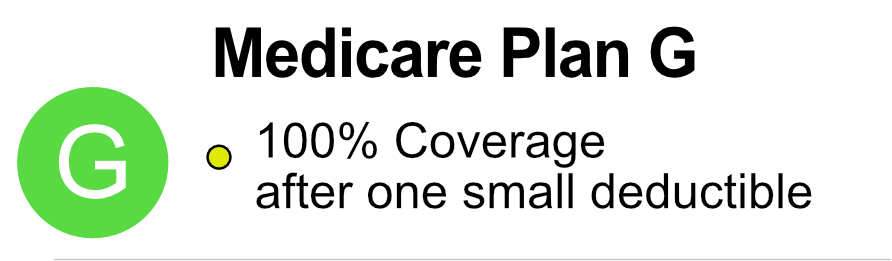

- Medicare Plan G

- Medicare Plan N

- Medicare Plan F

Medigap Plan F

Medicare Supplement Plan F is the most comprehensive plan available. It covers all of the gaps in Original Medicare, including:

- Part A deductible

- Part B deductible

- Part A coinsurance for hospital stays

- Part B coinsurance or copayment

- Skilled nursing facility care coinsurance

- Part A hospice care coinsurance or copayment

- Blood (first three pints)

- Foreign travel emergency care (limited)

- Part B excess charges

However, as of January 1, 2020, Plan F is no longer available for new Medicare beneficiaries. If you were eligible for Medicare before this date, you can still purchase Plan F if it is available in your area.

Medigap Plan G

Medicare Supplement Plan G is similar to Plan F, offering almost the same level of coverage. The only difference is that Plan G does not cover the Part B deductible. This plan is popular for its comprehensive coverage and lower premium compared to Plan F. Plan G covers:

- Part A deductible

- Part A coinsurance for hospital stays

- Part B coinsurance or copayment

- Skilled nursing facility care coinsurance

- Part A hospice care coinsurance or copayment

- Blood (first three pints)

- Foreign travel emergency care (limited)

- Part B excess charges

Medigap Plan N

Medicare Supplement Plan N is another popular option, offering slightly lower coverage than Plan G but with a lower premium.

Plan N has similar coverage to Plan G, except:

- On Plan N there could be up to a $20 copay for doctor’s visits (Telehealth visits do not apply)

- There is a $50 copay if you visit the ER and you’re not admitted (Urgent care centers are excluded)

Medicare Plan N does not cover Medicare Part B excess charges, which means you may need to pay out-of-pocket for these costs though these are quite rare.

However, the lower premium may offset these Medicare-approved expenses for some beneficiaries.

How to Enroll in a Medigap Plan

Enrolling in a Medigap plan is a straightforward process. Follow these steps to ensure a seamless enrollment experience:

- Determine your eligibility: You must be enrolled in Medicare Part A and Part B to be eligible for a Medigap plan. You cannot have a Medicare Advantage plan and a supplement plan simultaneously.

- Choose the right plan: Review the coverage and benefits of each plan and select the one that best suits your needs and budget.

- Find a provider: Medicare Supplement plans are offered by private insurance companies. Compare the premiums, customer service, and reputation of multiple providers before making a decision.

- Enroll during your Medigap Open Enrollment Period (OEP): The best time to enroll in a Medigap plan is during your OEP, which is a six-month period starting the month you turn 65 and are enrolled in Medicare Part B. During your OEP, you have a guaranteed issue right to enroll without medical underwriting, which means you cannot be denied coverage or charged higher premiums due to pre-existing conditions.

- Complete the application: Once you’ve chosen a provider and plan, complete the application process by providing the necessary information, including your Medicare number and the date your Part A and Part B coverage began.

- Pay the premium: Medicare Supplement plans require a monthly premium, which varies depending on the plan and provider. Make sure to pay your premium on time to maintain your coverage.

- Review your coverage annually: It’s essential to review your Medigap coverage annually to ensure it continues to meet your needs. If you decide to switch plans, be aware that medical underwriting may apply outside of your OEP, and you may be subject to higher premiums or denial of coverage based on your health status.

A Medicare Supplement insurance plan can provide essential financial protection for Medicare beneficiaries by covering out-of-pocket costs associated with Original Medicare. Understanding your options and enrolling in the right Medicare plan can give you peace of mind and help you manage your healthcare expenses. Remember to review your coverage annually and make any necessary adjustments to ensure it continues to meet your needs.

However, the lower premium may offset these Medicare-approved expenses for some beneficiaries.

Frequently Asked Questions

What exactly is Medigap?

Medigap, also known as Medicare Supplement Insurance, is private health insurance that covers certain out-of-pocket costs not covered by Original Medicare, such as deductibles, copayments, and coinsurance.

What are the different Medigap plans?

There are ten different Medigap plans available in most states: A, B, C, D, F, G, K, L, M, and N. Each plan offers a different combination of benefits, allowing you to choose based on your specific health needs and budget. There is also a High-deductible version of both Plan F and Plan G.

What is the purpose of Medigap plans?

Medicare Supplement Insurance is designed to help fill the gaps in Original Medicare coverage by covering out-of-pocket costs such as deductibles, co-payments, and coinsurance.

How much does Medigap cost?

The cost of a Medigap policy depends on several factors, including the specific plan, the insurance company, your location, and sometimes your age and health status.

Can I have Medigap and Medicare Advantage?

No, you can’t have both a Medigap policy and a Medicare Advantage plan. You can use a Medigap policy to supplement Original Medicare, but not Medicare Advantage.

What’s the difference between Medigap and Medicare Advantage?

Medigap and Medicare Advantage are both ways to supplement Original Medicare, but they work differently. Medigap is insurance that pays after Medicare pays its share of your healthcare costs. Medicare Advantage, on the other hand, is an alternative way to get your Medicare benefits, typically offering additional benefits like vision and dental care.

How do I choose between Medigap and Medicare Advantage?

The right choice depends on your healthcare needs, your budget, and your preferences. Consider factors like the cost, the coverage, whether your preferred doctors are in the plan’s network (for Medicare Advantage), and whether you travel frequently (Medigap provides coverage anywhere in the U.S. that accepts Medicare).

When can I enroll in a Medigap plan?

The best time to enroll in a Medigap plan is during your six-month Medigap Open Enrollment Period, which starts the first month you’re 65 or older and enrolled in Medicare Part B. During this time, you can buy any Medigap policy sold in your state, even if you have health problems.

Can I switch Medigap plans?

Yes, you can switch Medigap plans. However, if you apply after your Medigap Open Enrollment Period, the insurance company can use medical underwriting and may charge you more or deny coverage based on your health.

Do Medigap plans cover prescription drugs?

Medigap plans sold to new enrollees do not cover prescription drugs. If you need prescription drug coverage, you can join a Medicare Prescription Drug Plan (Part D).

Can anyone enroll in a Medigap plan?

To be eligible for a Medigap plan, you must be enrolled in both Medicare Part A and Part B. You cannot have a Medicare Advantage plan and a supplement plan simultaneously.

Will my Doctor accept my Medigap Plan?

As long as your doctor accepts Medicare patients, they will also accept your Medigap Plan. Doctors have a Medicare contract that obligates them to accept all Medigap insurance from all insurance companies. they are not allowed to pick and choose which ones they want to accept.

Do Medigap plans cover dental, vision, or hearing services?

No, Medigap plans do not cover dental, vision, or hearing services. These services are not covered by Original Medicare, and supplement plans are only designed to supplement Original Medicare coverage.

Do all insurance companies charge the same premium for the same Medigap plan?

No, premiums for Medigap plans can vary between insurance companies. It’s essential to compare multiple providers before choosing a plan to ensure you get the best value for your money.

Can my Medigap plan be canceled if my health changes?

No, as long as you pay your premiums on time and the plan is not discontinued, your Medigap coverage cannot be canceled due to changes in your health.

Finding the Right Medigap Plan

Finding the right Medigap plan is easier than you might think if you have help. Whether it’s a Medigap plan, or you have questions about Medicare Advantage or Medicare Part D, we’re here to answer all of your questions.

Call us today at 1-888-891-0229 and one of our knowledgeable, licensed insurance agents will be happy to assist you!

Russell Noga is the CEO and Medicare editor of Medisupps.com. His 15 years of experience in the Medicare insurance market includes being a licensed Medicare insurance broker in all 50 states. He is frequently featured as a featured as a keynote Medicare event speaker, has authored hundreds of Medicare content pages, and hosts the very popular Medisupps.com Medicare Youtube channel. His expertise includes Medicare, Medigap insurance, Medicare Advantage plans, and Medicare Part D.